When the implosion of Archegos Capital blew a hole worth more than $10bn out of a clutch of banks, one line in the biography of founder Bill Hwang stood out: Tiger Management.

Prior to the private investment firm’s collapse in March, Hwang was an obscure figure better known for his guilty plea to wire fraud charges in 2012. Fellow investors were stunned he could have emerged from that to secure $50bn in borrowing from heavy-hitting banks to supercharge what proved to be ill-fated bets.

But his pedigree as a former Tiger fund manager placed Hwang —

— who worked at New York-based Tiger Management from 1996 to 2001 — among hedge fund royalty. It meant that he had learnt his craft at a group famed for spectacular returns and concentrated equities bets as protégés of 1980s hedge fund pioneer Julian Robertson. The fiasco at Archegos underlines how, decades after shutting Tiger to outside investors, Robertson’s so-called Tiger Cubs still have the cachet to open doors to the world’s most prestigious banks and investors.

“If you come from a Tiger pedigree, it helps convince anyone to do business with you,” said a prime broker at one of the banks that lost money from the Archegos collapse.

Hwang is very much the exception that proves the rule in a group of managers that has made billions of dollars for clients. Some are now among the world’s most highly rated investors.

“No shop in the history of investment management has produced more phenomenal people,” said Dixon Boardman, chief executive of Optima Asset Management, who worked with Robertson at broker Kidder, Peabody & Co before Robertson set up Tiger in 1980.

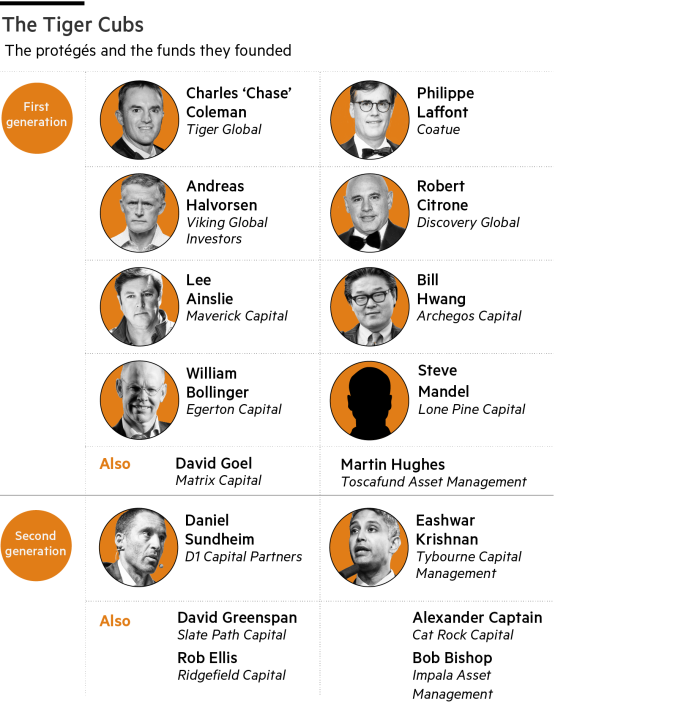

Tiger’s influence is scattered across global finance. Close to 200 hedge fund firms can trace their origins back to Tiger Management, according to investor LCH Investments. They are linked either through time at the original hedge fund, the 50 or so groups where Robertson provided seed capital to launch their businesses or as so-called ‘grandcubs’ that broke away from alumni firms. Only George Soros’s hedge fund Soros Fund Management comes close to having incubated so many key players in the industry, according to LCH.

Even now, the bond between Robertson and his charges remains strong, and they often hold similar positions. “Bill [Hwang] is a good friend, and I know Bill well. I think he made a mistake and I expect that he’s coming out of it and he’ll go right on,” Robertson, 88, told the Financial Times in a rare interview.

Did Hwang’s distinguished Tiger pedigree help convince banks to lend him so much money? “I don’t know,” said Robertson. “I just can’t answer that question.” Hwang declined to comment for this story.

Tiger’s record was exceptional, with 14 years of beating the US market, driven by eye-catching trades such as shorting copper as it slumped in 1996 or betting against the Thai baht the following year. It delivered average annual returns of more than 25 per cent net of fees between 1980 and 2000, when it gave back investor capital. Robertson refused to embrace internet stocks during the late 1990s dotcom boom and lost 19 per cent in 1999 — before his view was ultimately proved right.

“In a weird way Julian Robertson touches trillions of dollars of assets under management because there are so many people who worked for him directly [or] indirectly”, said Daniel Strachman, author of Julian Robertson: A Tiger in the Land of Bulls and Bears.

Some commentators argue the aura around the Tiger Cubs was hyperbole or has dimmed in recent years, and some methods pioneered in the early days at Tiger Management are now commonplace. Of late, for instance, many of these managers have been bullish on US growth stocks — a consensus trade during a period when unprecedented monetary easing drove equity markets higher.

But few can question the success of some of the original cubs.

“The success rate of the total universe is not that far off the success rate of the hedge fund community,” said Jim Neumann, chief investment officer at Sussex Partners, which advises clients on hedge fund investments. “But those that have been successful for the longer term have been extraordinarily successful and resilient to changing markets.”

Laying ‘the King’s table’

Many of the cubs remain good friends both with each other and with Robertson, and have developed similar investing styles they learnt from him. It is a deceptively simple approach: using fundamental research to buy the best companies and bet against the worst.

Robertson told the FT that a rigorous hiring process was key: “I think they were talented people and we went after them in a very deliberate and planned way,” he said. “They were really picked very carefully.”

Philippe Laffont, founder of Coatue Capital, one of the most prominent Tiger Cubs with $50bn under management, said Tiger’s focus on hiring “people who were well-rounded instead of specialists” was the “special sauce” that “created a culture of people who were competitive, curious and extroverted”.

A key player in that process was Dr Aaron Stern, a psychoanalyst who worked in various roles at the firm including chief operating officer for 30 years. Dr Stern, who died in April aged 96, was a leading expert in narcissistic personality disorder and wrote the influential 1979 book Me: The Narcissistic American.

“Aaron was a great, great man,” said Optima’s Boardman. “It would be too much to say he was responsible for Julian’s success . . . But he was the one who sorted out who should be there, who should be at the king’s table.”

Robertson used Dr Stern in the early 1990s to develop a systematic way of replicating Tiger Management’s early success hiring talented young analysts, which had until then relied on Robertson’s gut instinct. The test for applicants consisted of about 450 questions and lasted over three hours.

“He was very important because he really did perfect . . . this recruitment technique that we used,” said Robertson.

Questions could include the Rorschach test, developed in 1921 for spotting mental imbalances. Stern also designed the exams so applicants could not ‘game’ them by giving answers they thought Tiger wanted.

“Some of the questions were open-ended,” said one former portfolio manager who took the test. “It was along the lines of: Is it more important to get on well with your team or to challenge them? Would you prefer to be intellectually right but lose money or to be intellectually wrong but save the trade?”

The aim was to identify how applicants thought, took risks or worked in teams. The process was a product of its age; recruits were overwhelmingly male and there are no notable ‘tigresses’ in what remains to this day a heavily male industry. Still, the thought process stood out as quirky. Rather than just trying to find the most intelligent people, Tiger looked for people who were highly competitive and had excelled in fields such as sport.

“Once somebody had a certain amount of IQ, it really wasn’t as relevant as you think to their success”, said Alex Robertson, Julian’s son and president of Tiger Management today.

Two sides of the coin

Younger analysts worked alongside more experienced peers to learn their trade. Everyone worked hard, some doing up to 14-hour days and working on Saturdays. The firm built a gym, which Julian visited daily, on the top floor of its 101 Park Avenue headquarters to help employees work off stress.

“We were young and hyper-competitive analysts competing against people [in other firms] who worked seven-hour days and were used to two-martini lunches,” said Lee Ainslie, founder of Maverick Capital.

The firm was also keen to encourage analysts to informally share and challenge ideas, often walking into each other’s offices to debate the conclusion on a stock. Julian’s own corner office, a glass enclosure on the top floor, had no door — something designed to encourage his staff to pitch him.

“Early on Julian gave you the ability to focus on being intellectually honest,” said Coatue’s Laffont.

“For everything he forced you to see both sides of the debate. There were no zealots ever — every coin has two sides. If ever Julian thought that you had become dismissive of the other side of the story, then you were viewed as being unprepared — because you were viewed as being shortsighted or too narrow minded in your approach.”

Dr Stern also had a key role in resolving arguments among analysts and explaining how Julian ran the firm. “He was a great solutions person and problem solver,” said Alex Robertson. “He made sure that everybody stuck together as a team.”

Not all the cubs have gone on to become Vikings, Coatues or Tiger Globals. Aside from Hwang, who is described by one investor who met him at Tiger Management as being “very secretive” and “odd”, others such as Tom Facciola’s TigerShark and Scott Phillips’s Latimer Light have shut their doors in recent years.

And unlike Julian Robertson, Dr Stern was not universally liked within Tiger Management, said insiders. A strong and dominating personality, he could arouse resentment over the amount of influence he wielded over its founder. “Some people saw him as Julian’s horse-whisperer,” said one person close to the firm.

Stern “loved working along side” Robertson, particularly on philanthropic matters such as on medical research and educational reform, said Betty Lee, the psychoanalyst’s wife, who described the two as “longstanding” friends.

Long-term approach

Tiger Management and its cubs are known for their long-term outlook and in-depth research on companies, talking to customers and competitors to gain extra insight. Robertson’s aim was to find the best 20 stocks to buy and the worst 20 stocks to bet against by short selling. Tiger typically ran about 100 per cent leverage — meaning that gross market exposure could be up to 230 per cent.

While valuations were important, that could often be secondary to factors such as a company’s position in an industry and the barriers to entry. “The investment thesis was never built around whether a company would do well or badly over the next quarter,” said Laffont. “It was always a long-term focus, a three- to five-year time horizon.”

A similar approach has been taken by cubs such as Tiger Global’s Coleman, Laffont and Maverick’s Ainslie, whose backing of technology companies that could be considered expensive on traditional valuation metrics has yielded huge gains. All three have all expanded into private companies in pursuit of wider opportunities.

Investors who signed up with Coleman when he launched Tiger Technology, now Tiger Global, in 2001 at the age of 25 stand to have gained 43 times their initial investment. Coleman said that Robertson’s mentorship had given the cubs “the confidence to take risk when we identified unique opportunities”.

And David Goel’s low-profile Matrix Capital, which has raised only about $1bn from investors, has grown to roughly $7bn through performance gains, said people familiar with the firm.

“Julian Robertson’s ability to recruit young analysts, train them in equity investing and allow them to flourish as spin-off firms is unique, given the success that many of the Tiger Cubs have had,” Pierre-Henri Flamand, senior investment adviser to Man GLG, part of listed investment manager Man Group. “That will be his legacy.”

Timeline: The rise of Tiger Management

1980

Julian Robertson founds Tiger Management with about $8m in assets. By the end of the year it has made 54.9 per cent.

1987

After years of double-digit gains, Tiger hits a period of poor performance, eventually finishing the year down 1.4 per cent.

1991

Dr Aaron Stern joins Tiger.

1997

After years of strong gains, Tiger’s assets have risen to roughly $23bn.

1998

Tiger loses about $1.8bn because of turbulence in the dollar-yen market and finishes the year down 4 per cent.

1999

Tiger, which has shunned internet and technology stocks, shrinks to $8bn as performance suffers again, finishes the year down 19 per cent.

2000

Robertson says Tiger’s hedge fund will close.

Stay connected with us on social media platform for instant update click here to join our Twitter, & Facebook

We are now on Telegram. Click here to join our channel (@TechiUpdate) and stay updated with the latest Technology headlines.

For all the latest Education News Click Here

For the latest news and updates, follow us on Google News.